nCa Report

Editor’s Note: There are certain shortcomings in this report, mainly because quite a bit of the related information and data is not available on the net. Some of the information is behind the firewalls.

The difference in methodologies among the data sources is another factor.

For the collation and augmentation of information and for the general heavy lifting, we depend on various AI agents because we don’t have the human capacity to handle all of it on our own.

There is also the problem that e-commerce is not strictly and clearly defined as yet. There are many local transactions that should qualify as e-commerce but are not taken into account by the compilers of the data, mainly because there is no mechanism to collect such data (for example, local shopkeepers making home deliveries and receiving payments in cash, a legit e-commerce activity but undocumented).

In this report, we have not given the figure for the entire revenues of Kaspi.kz because there are conflicting sources but we are sure that the overall figure for the Kaspi.kz platform is substantially more than what we have mentioned in this report.

The data about the Internet penetration is approximation. The retail total online for Kazakhstan (16.6%) is an approximation. The data for Uzbekistan is perhaps understated.

On the whole, this report gives a pretty good picture of the state of e-commerce in Central Asia. Ed.

Key Points

- Rapid Regional Growth: The Central Asia e-commerce market reached approximately USD 14.7 billion in 2024, up from USD 11.1 billion in 2023, driven by increasing internet penetration (now over 80% in urban areas) and smartphone adoption. It seems likely that the sector will expand at a compound annual growth rate (CAGR) of around 30+% through 2033, potentially reaching USD 182 billion, though projections vary slightly across sources due to differing methodologies.

- Country Variations: Kazakhstan leads with the largest market , followed by Uzbekistan (USD 543 million in 2023, growing rapidly). Kyrgyzstan and Uzbekistan show strong momentum, while Tajikistan and Turkmenistan on the hard and soft infrastructure to catch up with the e-commerce boom. The progress made so far is commendable and there are opportunities for targeted investment.

- Key Trends: Cross-border trade, especially with Russia and China, is booming; digital wallets dominate payments (over 70% of transactions); and marketplaces like Wildberries are enabling local sellers to export. Challenges include logistics in landlocked areas and low digital literacy in rural zones (affecting 60% of the population), which could slow adoption if unaddressed.

- Projections with Caution: Over the next 5 years (to 2030), the regional market may hit USD 50-70 billion; by 10 years (2035), USD 100-150 billion; and 15 years (2040), exceeding USD 200 billion, assuming sustained infrastructure improvements. These estimates lean toward optimistic scenarios from market reports but acknowledge risks like geopolitical tensions and regulatory hurdles.

- Opportunities for Inclusion: E-commerce could create 500,000+ jobs by 2030, particularly for women and youth in rural areas, by bypassing traditional trade barriers. This figure is based on the projection of the current growth trend and, therefore, should be treated as an approximation. However, equitable growth requires harmonized regional policies to avoid widening urban-rural divides.

Market Overview

Central Asia’s e-commerce sector is at an inflection point, transforming from a nascent market into a dynamic hub. With a combined population of 75 million and rising GDP growth (projected at 4-5% annually), the region benefits from its strategic position between Europe, Russia, and China.

Internet penetration has surged to 77-87% in leading countries like Kazakhstan and Uzbekistan, fueling a shift from bazaar-based retail to digital platforms.

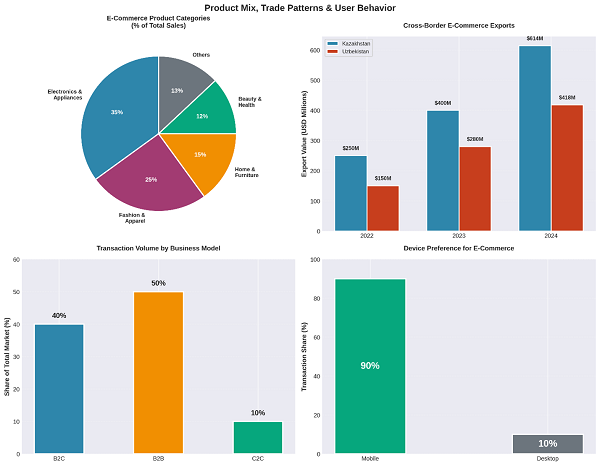

In 2024, business-to-consumer (B2C) transactions dominate (over 70%), with home appliances/electronics (35% share) and fashion (25%) as top categories.

Cross-border sales, particularly via Russian platforms, grew 50-80% year-over-year, highlighting export potential for local goods like textiles and agriculture.

Despite this, the sector accounts for just 4-16% of total retail (vs. 20-30% globally), indicating untapped potential.

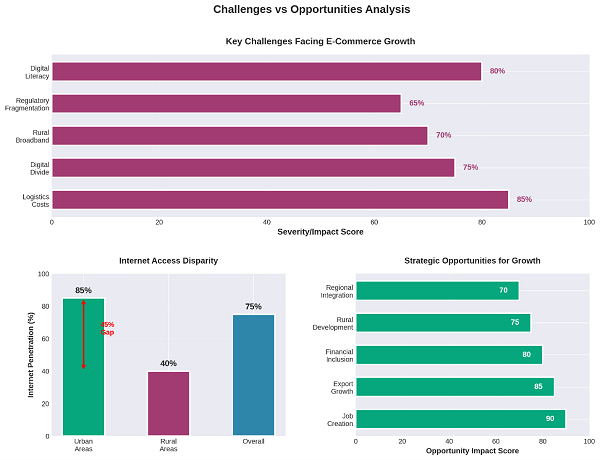

Government initiatives, such as Uzbekistan’s E-Commerce Strategy 2023-2027 and Kazakhstan’s Digital Kazakhstan program, are accelerating adoption through tax incentives and digital literacy campaigns. However, landlocked geography adds 20-30% to logistics costs, and only 40% of rural households have reliable broadband, limiting reach.

Country-Specific Trends and Turnover

E-commerce growth varies by country, with Kazakhstan as the regional anchor. Turnover data reflects recent surges, often 40-80% annually, driven by marketplaces and mobile apps.

| Country | 2023 Turnover (USD) | 2024 Turnover (USD) | YoY Growth (2023-2024) | Key Drivers |

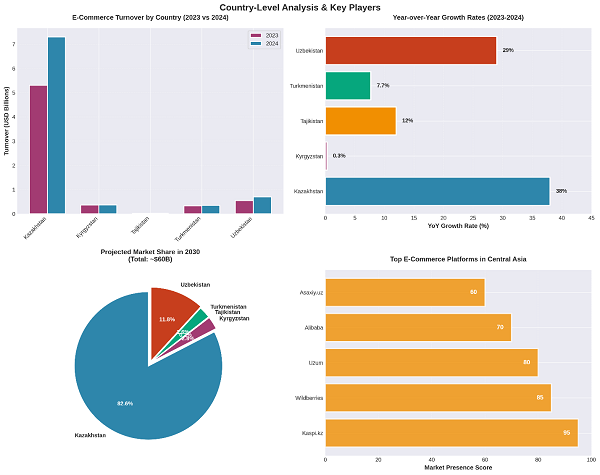

| Kazakhstan | 5.3 billion | 7.3 billion | 38% | Kaspi.kz dominance; 16.6% retail share |

| Kyrgyzstan | 359 million | 360 million | ~0-5% (stable) | Wildberries exports; mobile payments rise |

| Tajikistan | ~20 million | 22.4 million | 5% | Emerging laws; low penetration (4%) |

| Turkmenistan | ~325 million | Limited data (~350m est.) | 12% (projected) | Hard and soft infrastructure developing; potential in cross-border |

| Uzbekistan | 543 million (or 1bn varying est.) | ~700m est. | 30-40% | Uzum unicorn status; 4% retail share |

Kazakhstan: The market leader, with 91 million transactions in 2024. Platforms like Kaspi.kz (30 million monthly users) integrate banking and shopping, boosting average order values to USD 50. Exports via Wildberries tripled to USD 614 million.

Kyrgyzstan: Steady growth to USD 360 million, with 15,000 sellers on Wildberries generating USD 115 million. Rural challenges persist, but the E-Commerce Development Programme 2023-2026 aims for 15% annual increases.

Tajikistan: Nascent at USD 22 million, but the 2022 E-Commerce Law and World Bank support signal 13% CAGR. Digital wallets hit 10.4 million users in 2024, up 16%.

Turkmenistan: Projections at USD 325 million in 2023 growing 12% annually. Local platforms growing. Regional hubs could spur 20% growth by 2030.

Uzbekistan: Explosive, from USD 201 million in 2021 to USD 543 million in 2023. Over 50 marketplaces contribute USD 300 million annually; Uzum’s buy-now-pay-later (BNPL) model suits low-income users.

Regional total: USD 11.1 billion (2023) to USD 14.7 billion (2024), with B2B transactions at 50% share.

Main Players in the Sector

The landscape mixes local innovators with Russian/Chinese giants, enabling cross-border reach. Marketplaces hold 80-90% share.

- Kazakhstan: Kaspi.kz (USD 2.1 billion revenue; NASDAQ-listed, USD 20 billion cap); Wildberries (USD 614 million sales); Mechta.kz, Halyk Market.

- Kyrgyzstan: Wildberries (15,000 local sellers); Arena.Xspace; local apps like Madly.

- Tajikistan: Emerging players like Somon.tj; Wildberries entering 2025; NOVICA, eBay for exports.

- Turkmenistan: Growing; state-linked platforms; potential Wildberries expansion.

- Uzbekistan: Uzum (unicorn, USD 1 billion valuation; 800,000+ items); Wildberries (USD 418 million Uzbek sales); Asaxiy.uz, OLX, BirBir (classifieds, USD 10 million investment).

International: Alibaba/Taobao (free shipping pilots); AliExpress (cross-border leader). These platforms onboarded 50,000+ regional sellers in 2024, with Wildberries planning Tajik entry.

Transaction Methods: Gateways and Currencies

Consumers favor cash-on-delivery (COD, 40-50% in rural areas) and digital wallets (60-70%), reflecting trust issues and cash habits. Cards (Visa/Mastercard) are 20%, growing with BNPL.

- Gateways: Local systems like Click/Payme (Uzbekistan, acquired by TBC Bank); Kaspi Pay (Kazakhstan); Eskhata Online (Tajikistan). International: PayPal (limited); Qiwi, WebMoney for Russia ties. Blockchain pilots in Kyrgyzstan for remittances.

- Currencies: Local (KZT, UZS, KGS, TJS, TMT) for domestic; USD/RUB for cross-border (80% of exports). Multi-currency support on platforms like Uzum (14+ options) reduces conversion fees (2-5%).

- Trends: 16% YoY rise in cashless transactions; wallets like Payme process 70% in Uzbekistan. Challenges: Rural banking gaps; opportunities in CBDC pilots (e.g., Tajikistan’s e-som).

Projections for Growth

Forecasts assume 25-30% CAGR regionally, tempered by infrastructure needs. Country-level varies by digital readiness.

| Period | Regional Projection (USD Billion) | Kazakhstan (USD Billion) | Kyrgyzstan (USD Million) | Tajikistan (USD Million) | Turkmenistan (USD Million) | Uzbekistan (USD Billion) |

| Next 5 Years (2030) | 50-70 | 15-20 | 600 | 30-40 | 500-600 | 2-3 |

| Next 10 Years (2035) | 100-150 | 30-40 | 1,000 | 50-70 | 800-1,000 | 5-7 |

| Next 15 Years (2040) | 200+ | 50+ | 1,500+ | 100+ | 1,200+ | 10+ |

Regional: USD 182 billion by 2033 (IMARC); aligns with 32% CAGR to USD 147 billion by 2032. Drivers: 90% mobile penetration by 2030. Country Notes: Kazakhstan targets 20% retail share by 2030; Uzbekistan 15% growth via unicorn expansions; others via regional hubs (e.g., Manas Airport e-commerce park in Kyrgyzstan).

Additional Insights

Challenges: Logistics (high costs in mountains); digital divide (60% rural offline); regulations (fragmented taxes). Geopolitics risks 10-15% growth dips.

Opportunities: Job creation (e.g., 100,000 for women via platforms); exports ; sustainability (green logistics pilots). World Bank E-GATE program facilitated USD 23 million intra-regional trade in 2024.

Policy Recommendations: Harmonize standards (ISO for “Made in Central Asia”); invest USD 1-2 billion in broadband; train 1 million in digital skills by 2030.

Sustainability: Platforms like Uzum’s BNPL reduce debt stigma; AI for personalized rural delivery could cut emissions 20%.

In-Depth Analysis: The Evolving Landscape of E-Commerce in Central Asia

Central Asia’s e-commerce ecosystem is a compelling case study in digital transformation amid geographic and socioeconomic constraints. Encompassing Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan, the region—home to 75 million people and a youthful demographic (over 50% under 30)—is leveraging its Silk Road legacy to bridge East-West trade digitally.

As of 2024, the market’s USD 14.7 billion valuation reflects a 32% year-over-year surge from 2023’s USD 11.1 billion, outpacing global averages (9.4%). This growth, detailed in IMARC Group’s comprehensive reports, stems from a confluence of factors: smartphone penetration exceeding 100% in urban Kazakhstan and Uzbekistan, government-backed strategies like Digital Uzbekistan 2030, and the influx of Russian platforms amid post-2022 sanctions dynamics.

Yet, this expansion is not uniform. Kazakhstan’s mature ecosystem contrasts with Tajikistan’s embryonic stage, underscoring a digital divide that could exacerbate inequalities if unmitigated.

The World Bank’s E-GATE initiative, launched in 2023 with UK funding, has already catalyzed USD 23 million in B2B deals—over half intra-regional—demonstrating e-commerce’s role in fostering functional regionalism.

Below, we dissect trends, players, mechanics, forecasts, and broader implications, drawing on PwC, KPMG, and Statista data for a holistic view.

Historical Context and Current Turnover Dynamics

E-commerce in Central Asia traces to early 2000s pilots in Kazakhstan, accelerating post-2015 with mobile internet booms. By 2022, the market hit USD 8 billion (IMARC), ballooning to USD 14.7 billion in 2024 amid COVID-19’s lasting digital shift.

Turnover growth reflects this:

- Kazakhstan: From 2.4 trillion KZT (USD 5.3 billion) in 2023 to 3.4 trillion KZT (USD 7.3 billion) in 2024, per PwC’s Q1-Q4 analysis—a 42% rise, with marketplaces at 91% share. First-half 2024 saw 61% growth, per PwC, with 16.6% of total retail online.

- Kyrgyzstan: USD 359 million in 2023 to USD 360 million in 2024 (ECDB), stable but poised for 13.5% CAGR to USD 596 million by 2028 via UNDP-supported hubs.

- Tajikistan: USD 17-20 million in 2023 to USD 22.4 million in 2024 (ECDB/Statista), with 5% growth; digital wallets surged 16% YoY to 10.4 million.

- Turkmenistan: Data estimates USD 325 million in 2023 (Statista), projecting 12.5% CAGR; regional spillovers offer upside.

- Uzbekistan: USD 543 million (or USD 1 billion per Forbes) in 2023 to ~USD 700 million in 2024 (KPMG/Daryo), with 30-47% CAGR; 50+ platforms drive USD 300 million turnover.

Aggregately, B2B holds 50%, B2C 40%, with electronics (35%) and apparel (25%) leading categories. News Central Asia (nCa) reports Uzbekistan’s 2023 volume at USD 1 billion (4% retail), Kyrgyzstan at USD 360 million. Caspian Post estimates regional 2023 at under USD 6.5 billion, aligning with IMARC’s trajectory.

Profiling Key Players: Local Innovators and Global Entrants

The sector’s vibrancy lies in a hybrid model: domestic “super-apps” integrating finance and retail, alongside Russian/Chinese invaders capitalizing on sanctions and Belt-Road ties.

| Player | Country Focus | Key Metrics (2024) | Unique Edge |

| Kaspi.kz | Kazakhstan | USD 2.1B revenue; 30M monthly users | Fintech-ecom hybrid; NASDAQ-listed |

| Uzum | Uzbekistan | USD 1.6B valuation; 800K items | BNPL for Muslim consumers; unicorn |

| Wildberries | Region-wide | USD 614M Kazakhstan sales; 15K Kyrgyz sellers | Export enabler; Tajik entry 2025 |

| Mechta.kz | Kazakhstan | Top-3 marketplace | Local logistics focus |

| Asaxiy.uz | Uzbekistan | Classifieds leader | P2P emphasis |

| Somon.tj | Tajikistan | Emerging portal | Local adaptation |

| Arena.Xspace | Kyrgyzstan | Regional exporter | SME onboarding |

Wildberries dominates cross-border (USD 418M Uzbek sales), per Forbes Kazakhstan, while Alibaba’s “Made in Uzbekistan” section on Alibaba.com aids 300+ firms. Uzum’s 23x growth (2022-2023) exemplifies local scalability; BirBir’s USD 10M funding signals classifieds’ rise.

Globally, eBay/NOVICA support crafts exports, per World Bank consultations.

Transaction Ecosystems: Gateways, Currencies, and Behaviors

Payments blend legacy cash reliance with digital leaps, with 70% via wallets per Statista. COD persists (40%) for trust-building, but cashless rose 16% in Tajikistan alone.

- Popular Gateways: Payme/Click (Uzbekistan, 70% share post-TBC acquisition); Kaspi Pay (Kazakhstan, integrated); Eskhata/Qiwi (Tajikistan/Russia links). Emerging: Blockchain for remittances (Kyrgyzstan UNDP pilots).

- Currencies: Domestic primacy (e.g., UZS for 80% Uzbek transactions); USD/RUB for 80% exports. Platforms like Uzum support 14 currencies, minimizing 2-5% FX fees.

- Conduct: Mobile-first (90% transactions); social media orders (50% via Telegram/Facebook, per World Bank surveys). BNPL (Uzum’s shariah-compliant) aids low-income access; fraud controls via 3D Secure.

Challenges: Rural unbanked (40%); opportunities: CBDC integration could halve cross-border costs by 2030.

Forward-Looking Projections: Scenarios to 2040

IMARC forecasts USD 182.2 billion by 2033 (30.6% CAGR from 2025), with Kazakhstan at 40% regional share. ECDB/Statista extend to 2028-2029, implying:

- 2030 (5 Years): USD 50-70 billion regionally; Uzbekistan hits USD 2-3 billion via 41-47% CAGR (KPMG).

- 2035 (10 Years): USD 100-150 billion; Kyrgyzstan USD 1 billion if hubs succeed.

- 2040 (15 Years): USD 200+ billion; Turkmenistan USD 1.2 billion with liberalization.

Uncertainties: 10-15% downside from geopolitics; upside from E-GATE’s USD 21 million MSME deals scaling to USD 100 million annually. Penetration could reach 20% retail by 2030 (Kazakhstan target).

Challenges, Opportunities, and Strategic Imperatives

Challenges (per World Bank/KPMG): Infrastructure (broadband at 40% rural); literacy (60% offline); logistics (540% “tariff” equivalent for landlocked trade); fragmented regs (e.g., varying VAT). Cyber risks exposed 422 million records globally in Q3 2024.

Opportunities: 500,000 jobs by 2030 (women/youth focus); USD 4.37 billion AI-logistics investments; “Made in Central Asia” branding via ISO harmonization. E-GATE’s 70 new markets for MSMEs exemplify poverty alleviation potential.

Recommendations: Regional standards body; USD 1 billion broadband fund; skills academies (1 million trainees). Sustainability: Green delivery could cut emissions 20%; inclusive BNPL for 40% unbanked.

E-commerce is, arguably, Central Asia’s economic equalizer, with balanced growth hinging on collaborative reforms. /// nCa, 16 October 2025

Key Citations

- IMARC Group: Central Asia E-Commerce Market 2025-33

- IMARC Group: Central Asia E-Commerce to 2032

- News Central Asia: E-Commerce Trends 2025

- IMARC: Central Asia E-Commerce 2023 Report

- PwC: Kazakhstan Retail E-Commerce 2024

- ECDB: Kyrgyzstan E-Commerce

- ECDB: Tajikistan E-Commerce

- Statista: Turkmenistan E-Commerce

- Daryo News: Uzbekistan E-Commerce Surge

- Kun.uz: Uzbekistan E-Commerce 2024

- Caspian Post: Central Asia E-Hub

- KPMG: Uzbekistan E-Commerce 2023

- World Bank: E-GATE Program

- World Bank Blog: Poverty via E-Commerce

- Statista: Kazakhstan E-Commerce

- Statista: Central Asia Digital Commerce

- KVY Technology: E-Commerce Asia 2024